Page 47 - Nexia SAB&T Property & Tax Guide 2022

P. 47

TRUSTS

TAX RATES

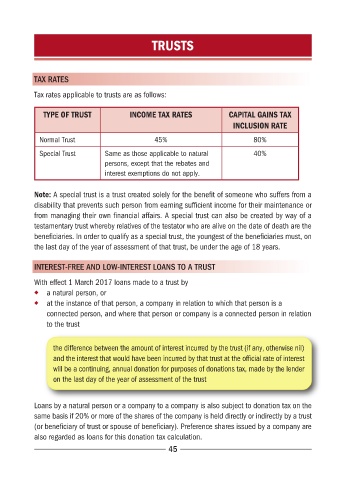

Tax rates applicable to trusts are as follows:

TYPE OF TRUST INCOME TAX RATES CAPITAL GAINS TAX

INCLUSION RATE

Normal Trust 45% 80%

Special Trust Same as those applicable to natural 40%

persons, except that the rebates and

interest exemptions do not apply.

Note: A special trust is a trust created solely for the benefit of someone who suffers from a

disability that prevents such person from earning sufficient income for their maintenance or

from managing their own financial affairs. A special trust can also be created by way of a

testamentary trust whereby relatives of the testator who are alive on the date of death are the

beneficiaries. In order to qualify as a special trust, the youngest of the beneficiaries must, on

the last day of the year of assessment of that trust, be under the age of 18 years.

INTEREST-FREE AND LOW-INTEREST LOANS TO A TRUST

With effect 1 March 2017 loans made to a trust by

◆ a natural person, or

◆ at the instance of that person, a company in relation to which that person is a

connected person, and where that person or company is a connected person in relation

to the trust

the difference between the amount of interest incurred by the trust (if any, otherwise nil)

and the interest that would have been incurred by that trust at the official rate of interest

will be a continuing, annual donation for purposes of donations tax, made by the lender

on the last day of the year of assessment of the trust

Loans by a natural person or a company to a company is also subject to donation tax on the

same basis if 20% or more of the shares of the company is held directly or indirectly by a trust

(or beneficiary of trust or spouse of beneficiary). Preference shares issued by a company are

also regarded as loans for this donation tax calculation.

45