Page 36 - Nexia SAB&T Property and Tax Guide 2025

P. 36

TRUSTS

TAX RATES

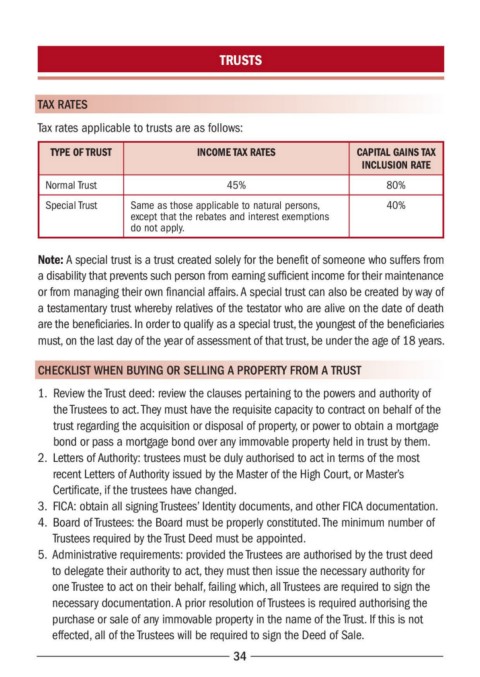

Tax rates applicable to trusts are as follows:

TYPE OF TRUST INCOME TAX RATES CAPITAL GAINS TAX

INCLUSION RATE

Normal Trust 45% 80%

Special Trust Same as those applicable to natural persons, 40%

except that the rebates and interest exemptions

do not apply.

Note: A special trust is a trust created solely for the benefit of someone who suffers from

a disability that prevents such person from earning sufficient income for their maintenance

or from managing their own financial affairs. A special trust can also be created by way of

a testamentary trust whereby relatives of the testator who are alive on the date of death

are the beneficiaries. In order to qualify as a special trust, the youngest of the beneficiaries

must, on the last day of the year of assessment of that trust, be under the age of 18 years.

CHECKLIST WHEN BUYING OR SELLING A PROPERTY FROM A TRUST

1. Review the Trust deed: review the clauses pertaining to the powers and authority of

the Trustees to act. They must have the requisite capacity to contract on behalf of the

trust regarding the acquisition or disposal of property, or power to obtain a mortgage

bond or pass a mortgage bond over any immovable property held in trust by them.

2. Letters of Authority: trustees must be duly authorised to act in terms of the most

recent Letters of Authority issued by the Master of the High Court, or Master’s

Certificate, if the trustees have changed.

3. FICA: obtain all signing Trustees’ Identity documents, and other FICA documentation.

4. Board of Trustees: the Board must be properly constituted. The minimum number of

Trustees required by the Trust Deed must be appointed.

5. Administrative requirements: provided the Trustees are authorised by the trust deed

to delegate their authority to act, they must then issue the necessary authority for

one Trustee to act on their behalf, failing which, all Trustees are required to sign the

necessary documentation. A prior resolution of Trustees is required authorising the

purchase or sale of any immovable property in the name of the Trust. If this is not

effected, all of the Trustees will be required to sign the Deed of Sale.

34