Page 47 - Nexia SAB&T Trust Guide 2022

P. 47

Other anti-avoidance provisions for trusts

Various anti-avoidance provisions exist to combat the use of trusts for income

splitting and tax avoidance schemes, including the deemed donation tax to be

levied on interest-free or low interest loans to trusts.

Income splitting occurs where the marginal rate of tax is reduced to an amount less

than if the income had been taxed from one source.

Section 103(2) of the Income Tax Act includes trusts – and prevents the utilisation

of any loss in a trust, solely for the purposes of avoiding tax.

The Section 7 deeming provisions of the Income Tax Act work mainly on the basis

whereby any income earned by the trust as a result of a donation, settlement,

or other disposition made by a person (“the donor”) which is not distributed, is

deemed to be the income of that donor and taxed in their hands. If income is

distributed to beneficiaries who are minor children of the donor, the income is also

taxed in the hands of the donor. Similar provisions exist in respect of capital gains

made by or accrued to a trust.

Withholding Tax on Acquisition of Property from Non-Resident

by a Trust

The purchaser (trust) must withhold CGT on the purchase price where immovable

property are purchased from a non-resident except where the amount payable by

the purchaser is less than R2 million. The amount withheld is an advance tax in

respect of the sellers’ liability for CGT. This withholding tax is not a final tax and is

merely a prepayment of the expected CGT.

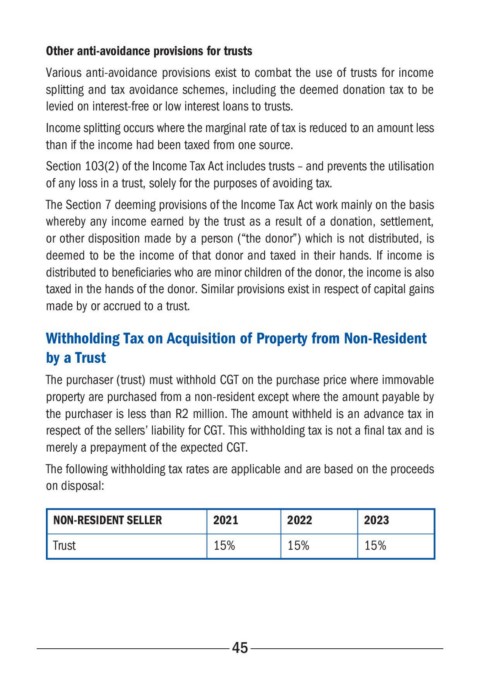

The following withholding tax rates are applicable and are based on the proceeds

on disposal:

NON-RESIDENT SELLER 2021 2022 2023

Trust 15% 15% 15%

45