Page 59 - Nexia SAB&T Estate Planning Guide 2024

P. 59

u The acquisition of a contingent right in a trust that holds a residential

property or the shares in a company or the member’s interest in a close

corporation which owns residential property comprising more than 50% of

its assets, is subject to transfer duty at the applicable rate.

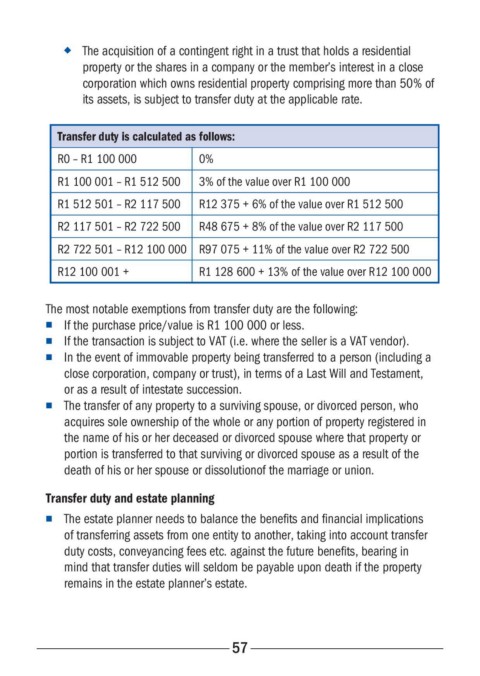

Transfer duty is calculated as follows:

R0 – R1 100 000 0%

R1 100 001 – R1 512 500 3% of the value over R1 100 000

R1 512 501 – R2 117 500 R12 375 + 6% of the value over R1 512 500

R2 117 501 – R2 722 500 R48 675 + 8% of the value over R2 117 500

R2 722 501 – R12 100 000 R97 075 + 11% of the value over R2 722 500

R12 100 001 + R1 128 600 + 13% of the value over R12 100 000

The most notable exemptions from transfer duty are the following:

n If the purchase price/value is R1 100 000 or less.

n If the transaction is subject to VAT (i.e. where the seller is a VAT vendor).

n In the event of immovable property being transferred to a person (including a

close corporation, company or trust), in terms of a Last Will and Testament,

or as a result of intestate succession.

n The transfer of any property to a surviving spouse, or divorced person, who

acquires sole ownership of the whole or any portion of property registered in

the name of his or her deceased or divorced spouse where that property or

portion is transferred to that surviving or divorced spouse as a result of the

death of his or her spouse or dissolutionof the marriage or union.

Transfer duty and estate planning

n The estate planner needs to balance the benefits and financial implications

of transferring assets from one entity to another, taking into account transfer

duty costs, conveyancing fees etc. against the future benefits, bearing in

mind that transfer duties will seldom be payable upon death if the property

remains in the estate planner’s estate.

57