Page 40 - Nexia SAB&T Property & Tax Guide 2022

P. 40

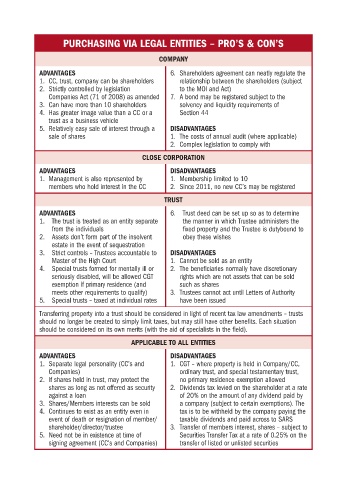

PURCHASING VIA LEGAL ENTITIES – PRO’S & CON’S

COMPANY

ADVANTAGES 6. Shareholders agreement can neatly regulate the

1. CC, trust, company can be shareholders relationship between the shareholders (subject

2. Strictly controlled by legislation to the MOI and Act)

Companies Act (71 of 2008) as amended 7. A bond may be registered subject to the

3. Can have more than 10 shareholders solvency and liquidity requirements of

4. Has greater image value than a CC or a Section 44

trust as a business vehicle

5. Relatively easy sale of interest through a DISADVANTAGES

sale of shares 1. The costs of annual audit (where applicable)

2. Complex legislation to comply with

CLOSE CORPORATION

ADVANTAGES DISADVANTAGES

1. Management is also represented by 1. Membership limited to 10

members who hold interest in the CC 2. Since 2011, no new CC’s may be registered

TRUST

ADVANTAGES 6. Trust deed can be set up so as to determine

1. The trust is treated as an entity separate the manner in which Trustee administers the

from the individuals fixed property and the Trustee is dutybound to

2. Assets don’t form part of the insolvent obey these wishes

estate in the event of sequestration

3. Strict controls – Trustees accountable to DISADVANTAGES

Master of the High Court 1. Cannot be sold as an entity

4. Special trusts formed for mentally ill or 2. The beneficiaries normally have discretionary

seriously disabled, will be allowed CGT rights which are not assets that can be sold

exemption if primary residence (and such as shares

meets other requirements to qualify) 3. Trustees cannot act until Letters of Authority

5. Special trusts – taxed at individual rates have been issued

Transferring property into a trust should be considered in light of recent tax law amendments – trusts

should no longer be created to simply limit taxes, but may still have other benefits. Each situation

should be considered on its own merits (with the aid of specialists in the field).

APPLICABLE TO ALL ENTITIES

ADVANTAGES DISADVANTAGES

1. Separate legal personality (CC’s and 1. CGT – where property is held in Company/CC,

Companies) ordinary trust, and special testamentary trust,

2. If shares held in trust, may protect the no primary residence exemption allowed

shares as long as not offered as security 2. Dividends tax levied on the shareholder at a rate

against a loan of 20% on the amount of any dividend paid by

3. Shares/Members interests can be sold a company (subject to certain exemptions). The

4. Continues to exist as an entity even in tax is to be withheld by the company paying the

event of death or resignation of member/ taxable dividends and paid across to SARS

shareholder/director/trustee 3. Transfer of members interest, shares – subject to

5. Need not be in existence at time of Securities Transfer Tax at a rate of 0.25% on the

signing agreement (CC’s and Companies) transfer of listed or unlisted securities