Page 7 - Nexia SAB&T Property & Tax Guide 2022

P. 7

TRANSFER DUTY ON IMMOVABLE PROPERTY

Transfer duty is an indirect tax on the acquisition of immovable property situated in South

Africa. The following are the main provisions:

◆ It is calculated on the value of the immovable property (purchase price or market value

whichever is the highest).

◆ It is payable within six months after the transaction is entered into.

◆ Where a registered VAT vendor purchases property from a non-vendor, the notional

input tax is calculated by multiplying the tax fraction [15/115 (14/114 before 1 April

2018)] by the lesser of the consideration paid or market value.

◆ The acquisition of a contingent right in a trust that holds a residential property or

the shares in a company or the member’s interest in a close corporation which owns

residential property comprising more than 50% of its assets, is subject to transfer duty

at the applicable rate.

Transfer duty is calculated as follows:

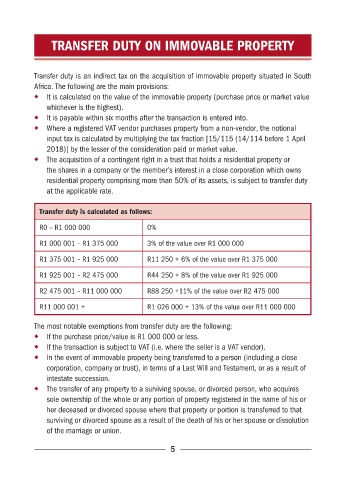

R0 – R1 000 000 0%

R1 000 001 – R1 375 000 3% of the value over R1 000 000

R1 375 001 – R1 925 000 R11 250 + 6% of the value over R1 375 000

R1 925 001 – R2 475 000 R44 250 + 8% of the value over R1 925 000

R2 475 001 – R11 000 000 R88 250 +11% of the value over R2 475 000

R11 000 001 + R1 026 000 + 13% of the value over R11 000 000

The most notable exemptions from transfer duty are the following:

◆ If the purchase price/value is R1 000 000 or less.

◆ If the transaction is subject to VAT (i.e. where the seller is a VAT vendor).

◆ In the event of immovable property being transferred to a person (including a close

corporation, company or trust), in terms of a Last Will and Testament, or as a result of

intestate succession.

◆ The transfer of any property to a surviving spouse, or divorced person, who acquires

sole ownership of the whole or any portion of property registered in the name of his or

her deceased or divorced spouse where that property or portion is transferred to that

surviving or divorced spouse as a result of the death of his or her spouse or dissolution

of the marriage or union.

5